-

Sector Focus

We specialise in the investment management industry offering audit, assurance, tax and corporate recovery and liquidation services.

-

Personal Tax Services

There are many tax rules that can affect you personally and therefore which will have an impact on your personal wealth.

-

QI Compliance

Qualified Intermediaries (QI) have to take action now to perform a Certification to the Internal Revenue Service (IRS).

-

Download our tax brochures

The Guernsey tax team at Grant Thornton aim to provide the island with a premier tax advisory service both to private clients and the Guernsey business community including the investment management industry.

-

Jersey Tax Return

A page with a link for Jersey Tax Returns

-

ESG

ESG can either be seen as a risk management tool or an opportunity, either way it is imperative to your business, whatever your size and whether you are listed or not.

-

Professional Services

Business and accounting support for professional services

-

Finance Industry

We work with a broad range of clients and their financial stakeholders, from entrepreneurs in the early days to fast growing and established businesses to public companies competing in global markets.

-

Local Businesses

Businesses come in many shapes and sizes – from innovative start-ups to long-established local businesses. But however large or small your business, the chances are you face similar challenges.

-

Corporate Insolvency

Our corporate investigation, Guernsey liquidation and recovery teams focus on identifying and resolving issues affecting profitability, protecting enterprise value and facilitating a full recovery where possible.

-

Corporate Simplification

Redundant corporate entities can over complicate group structures and waste thousands of pounds in unnecessary costs each year. 46% of the c.15,500 companies controlled by the FTSE100 are dormant and it is estimated that the average cost of administering dormant companies is between £3,500 and £5,000 per company, per year.

-

Debt Advisory

Our Debt Advisory team provides commercial and financial debt advice to corporate entities and public sector bodies in a range of sectors. Our engagements include advice on stand-alone transactions and solutions or as part of an integrated business plan, in both the project and corporate arenas.

-

Exit Strategy Services

We offer a tailored methodology designed to enable a company to be reviewed in a group context to assess ways to maximise its value.

-

Financial Restructuring

For companies challenged by under-performance we work with management teams, shareholders, lenders and other stakeholders to implement financial restructuring solutions creating a stable platform for business turnaround.

-

Strategic performance reviews

Strategic performance reviews analyse the key drivers of performance improvement. Our specialists utilise a framework to evaluate financial and operational options and to identify solutions for businesses and their stakeholders.

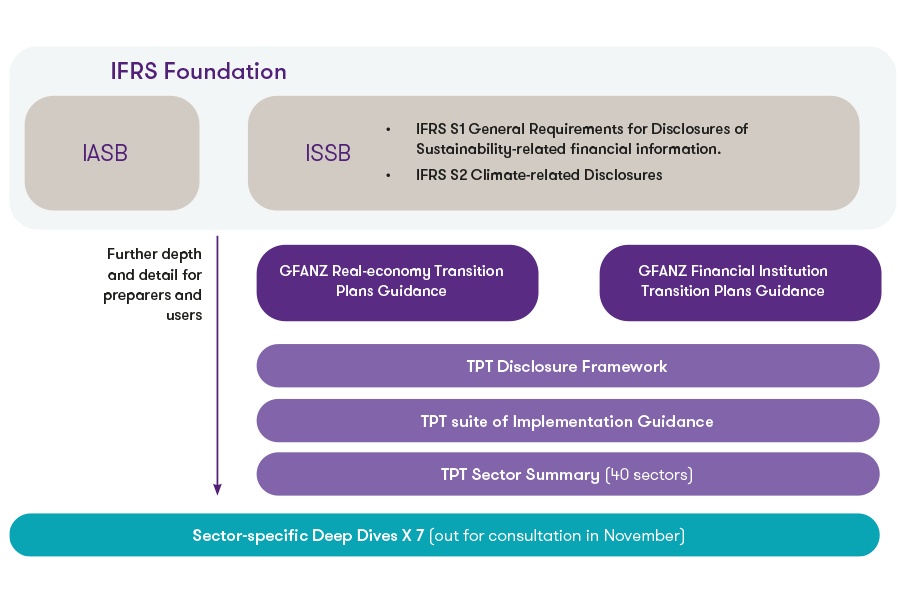

The TPT framework delivers this information via its good practice recommendations.

Although a UK Government initiative, the taskforce was made up of a variety of industry professionals.

The UK, alongside many other nations, have signed up to the 2050 net zero pledge. It is understood that the private sector will drive progress towards achieving the goal, and will therefore need to move quickest, and be under the most scrutiny. However, the private sector comprises businesses of all shapes, sizes and levels of maturity, hence the TPT is designed to be applicable to all and allow everyone to start their journey with the appropriate guidance in place.

The TPT guidance has been designed to ensure it aligns with existing guidance produced by the GFANZ as well as building upon the ISSB standards, see illustration below. The work is designed not to demonise, but support, with the creation of clear and credible plans.

What does it say:

In simple terms, it tells you how to produce a climate transition plan.

The TPT recommends disclosure of a company’s strategic climate ambition, and most importantly, how this will reflect in its governance, accountability, operational and financial plans.

The framework is split into 5 disclosure elements, which are:

- 1. Foundations

This element is aimed to show the core operations of the business and what its strategic ambition with regards to climate transition and decarbonisation is. An understanding of the business model and value chain needs to be detailed, to robustly determine the carbon emissions coming from operations. This will be key in understanding the approach to net zero, as scope 3 emissions typically contribute up to 95% of an organisations total emissions.

Finally, assumptions and external factors must be outlined. In the early stages of transition plan reporting, these will be numerous.

- 2. Implementation strategy

This section is very much detailed on the business itself. Its operations, products and services and policies and conditions. The focus being on whether the business understands its current carbon impact through it’s day-to-day running, and what plans it has to reduce this to achieve net zero status.

This must tie into financial planning, with a recognition of the financial costs and opportunities involved in re-orientating operations to a net zero future.

- 3. Engagement strategy

Here, businesses must focus on the external stakeholders and partners. Engagement with the value chain, industry, existing stakeholders and all others must be considered, and a plan of how to gain robust emissions data thought through.

Finally, transition risks such as engagement with Government, public sector bodies, communities and society as a whole must be thought through and reported.

- 4. Metrics and targets

The quantitative aspect begins in this disclosure element, as the reality of the carbon impact of the business, and its pathway to net zero become clear. Financial metrics and targets, alongside GHG metrics and targets must be reported. Likewise, the usage of carbon credits currently as well as going forward.

The governance, engagement and operation around this data must be outlined.

- 5. Governance

The role, competence, experience and know-how of the Board/management of the business, and how it is guiding its operations are detailed here. The oversight, accountability and reporting responsibilities of management, as well as the culture and direction it sets towards a net zero future should be reported. The skills and competencies of management and proof that they can accurately and competently steer a business into the new reality are key, of course noting that this is a transition, and therefore identified and targeted future training will be necessary.

Finally, there needs to be evidence that incentives and remuneration of management is tied to a net zero future, and the right structure is geared towards achieving this.

Why is it important:

As the global transition to a low carbon economy gathers pace, and importance, investors are demanding more robust and concise information on how businesses are adapting their operations to achieve ambitious net zero targets.

The TPT aims to provide forward-looking information, allowing investors to be much-better equipped to analyse a business’ prospects, and hence make more efficient investment decisions.

If (more likely when..) the TPT guidance is widely adopted and made a part of mandatory reporting, stakeholders will expect quality, audit-ready reporting to already be in place. To produce this kind of reporting will be no mean feat, and preparation needs to begin in earnest, NOW.

What do you need to do:

Act, now.

Many businesses of all sizes and industry are producing or actively working on their climate transition plans, to ensure they align with the UK target of net zero by 2050, at a minimum.

Firstly, the tone needs to be set at the top, and businesses must ensure their Board and/or management team understand the nature of the challenge, are experienced and competent in what needs to be done, and sets a strategy towards achieving it. This tone must then flow through the organisation, ensuring all staff are aware that reaching this goal is a part of their remit, and will require their help.

Collecting the data needed to accurately complete a climate transition plan will need the help of professional advisors and those experienced in doing this. Businesses must ensure this support is in place, and reporting is up to speed.

Will this make a difference?

All these signs say, yes. This is a groundbreaking framework, developed and supported by the key players in the public and private sector. It may not be right first time around, but the clear and undisputed direction of travel is towards businesses, of all sizes and industry, producing a climate transition plan as part of their usual package of financial reporting.

As the UK has been a first-mover, I would expect other jurisdictions to follow, quickly so as not to be left behind, with a global baseline emerging as the reporting becomes more commonplace.

What will good look like?

Look to the the biggest listed, global, firms who are well placed to produce this reporting, and have already invested in the infrastructure to do so.

A core part of the TPT was to make the framework applicable to businesses of all shapes and sizes, and subsequent education and awareness raising amongst the SME population will begin. This tells me that everyone will be expected to report, and report well, with no excuses given for poor disclosure as a result of all the attention the TPT has received.

Can the UK be a global leader?

Yes. Jurisdictions all over the world are grappling with decarbonisation and how to achieve it, this is no mean feat with the end game of the Paris commitments in sight in 2030. The UK have designed de-facto peer-reviewed and industry approved model for disclosing decision-useful climate information which assists all companies on the road to 2030.

There is always a risk, as is known within ESG circles, of conflicting global standards confusing companies, but the TPT is aware of this and has produced a domestic framework that is already compatible with global standards.

The TPT guidance has been designed to ensure it aligns with existing guidance produced by the GFANZ as well as building upon the ISSB standards.